- Qualcomm stock, like most of the stocks in the semiconductors industry, has been hit by a massive sell-off in the last year and has lost more than 30% of its capitalization since January 2022.

- Among the Big Cap sector, Everest Formula has recognized Qualcomm Inc. as one of the most interesting companies, which deserves an in-depth analysis.

- In this article, we will analyze the stock using the most important indicators of the Everest Analyzer and by calculating the stock’s intrinsic value with a Discounted Cash Flow model.

Are you interested in finding the best value stocks in each sector on your own? Premium members can use the Everest Screener to get the most valuable companies to invest in for each sector every day. Join now!

Introduction

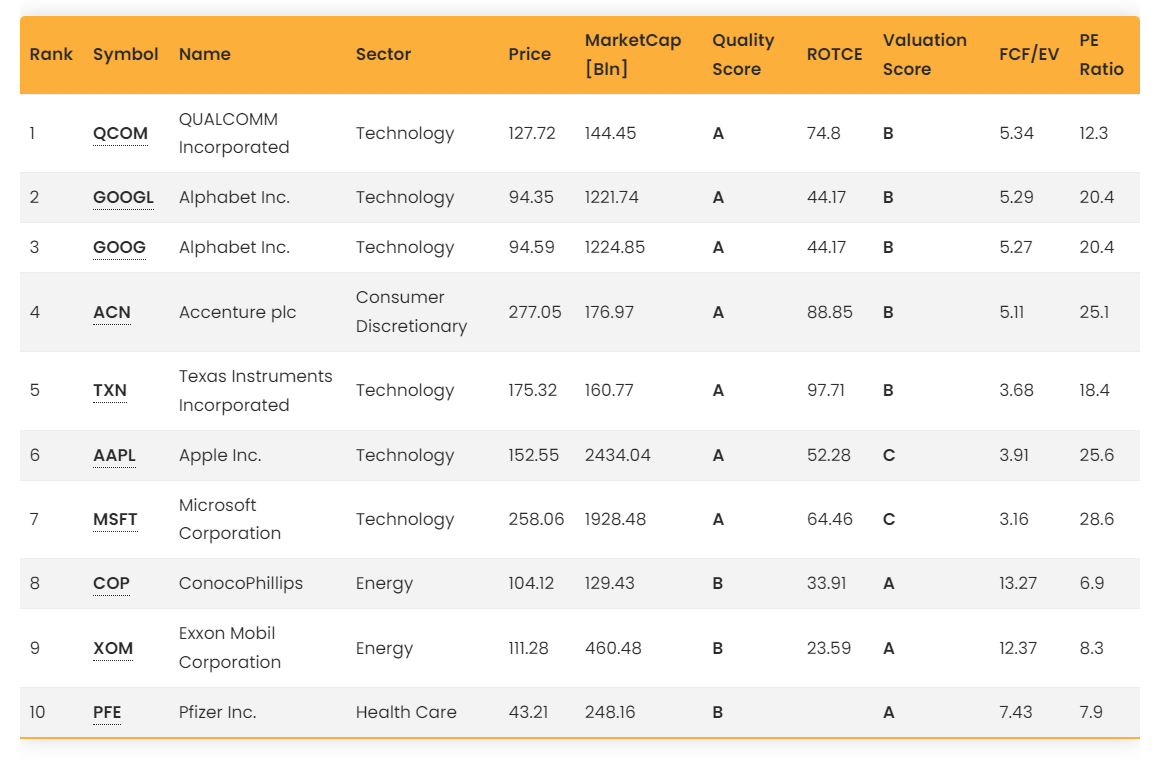

Looking at Everest Formula’s screener in the sector of large-capitalization companies (with a market cap greater than 100 billion dollars) in search of possible bargains in the market, we noticed that the first position is occupied by a semiconductor market leader, namely Qualcomm.

Qualcomm is a leading technology company that designs and manufactures semiconductor products and solutions for wireless communication, automotive, and internet of things (IoT) industries. The company is well known for its Snapdragon processors used in smartphones and other mobile devices, and it has a strong presence in the global market.

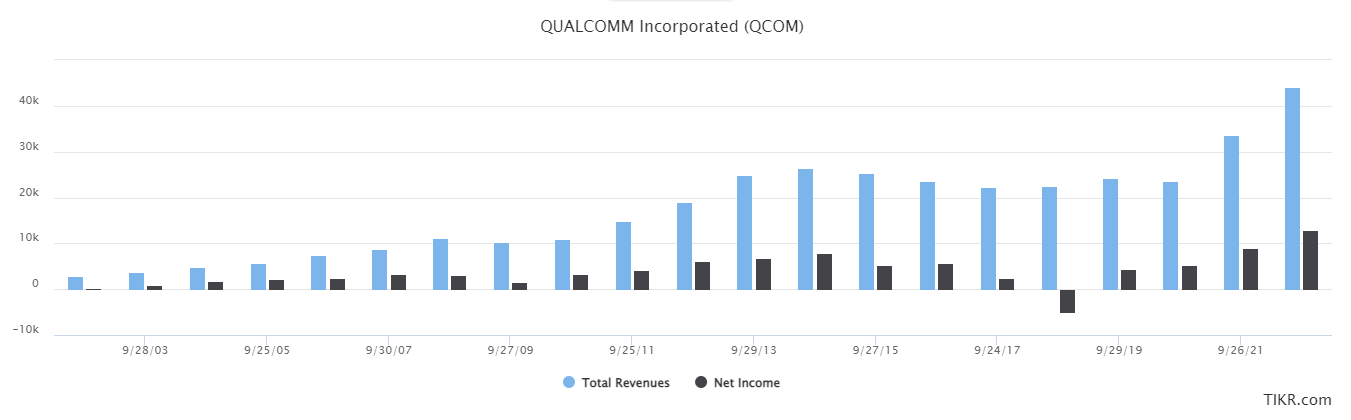

The company’s revenue has steadily increased over the past twenty years, reaching $44.2 billion in 2022, a 32% increase from the previous year. Similarly, the company’s net income increased, reaching $12.9 billion in 2022. Moreover, in terms of profitability, Qualcomm has a healthy operating margin of 33.7% and a net margin of 27.4%. As a result, Qualcomm’s financial performance is impressive, indicating that the company is well-positioned for growth in the future.

Despite that, Qualcomm has been hit hard in the last year. After a global chip shortage in 2021, demand has receded significantly. Sales for many big-ticket electronics, such as laptops and smartphones, have decreased considerably from last year’s record levels. As the stay-and-work-at-home trends have diminished, consumers are focusing their spending elsewhere, such as on travel and recreational goods. In addition, the inflationary wave has further hit consumer spending power for electronics.

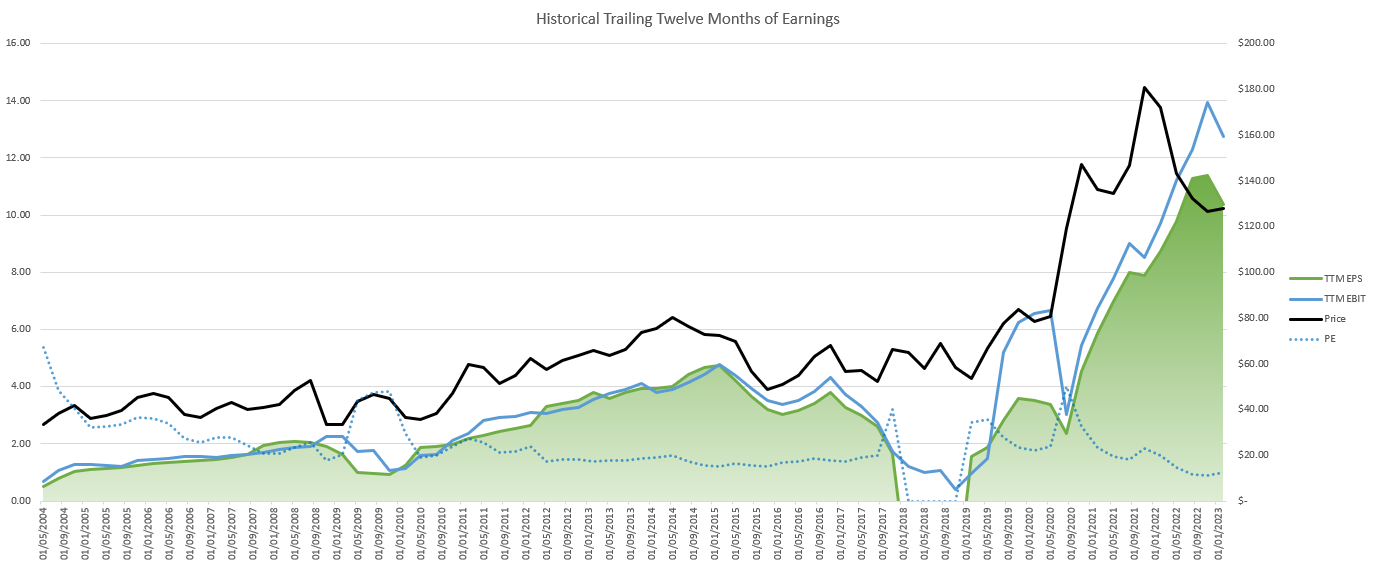

Now, let’s look at the historical earnings and prices for Qualcomm:

Qualcomm is a cyclical stock that experienced declining or negative earnings in its lifecycle. However, eventually, earnings have always bounced back from these declines and have typically done it in a reasonably timely manner. Moreover, every cycle over the past 20-year earnings has experienced a higher peak than the previous cycle. Therefore, we can infer that QCOM is in a secular growth trend, and even when earnings are declining and the price is falling (like now), QCOM cannot be considered a value trap. We can affirm that even because it is intuitive that in our society, the demand for chipsets and automotive/IoT software will increase in the next decade.

Investment thesis

Qualcomm is a solid and high-quality company that needs to be taken into consideration by investors for these key factors:

- Strong Market Position: Qualcomm is a market leader in the semiconductor industry, with a strong presence in the mobile device and IoT markets. Snapdragon processors are used in many of the world’s top smartphones, including Samsung’s Galaxy and Apple’s iPhone. Additionally, Qualcomm has partnerships with various companies, including General Motors, Ford, and Amazon, giving the company a foothold in the automotive and IoT industries.

- Financial Performance: Qualcomm has a solid financial performance and good management. Although cyclical, the company’s profitability has always been remarkably high, and the debt under control.

- Undervalued Stock: As we will see in the next section, Qualcomm’s current P/E ratio is lower than the industry average. The P/E ratio, together with other valuation ratios, suggests that the company’s stock is currently undervalued. In addition, Qualcomm has a healthy dividend yield of 1.91%, making it an attractive option for investors looking for income.

Risks

While Qualcomm’s financial performance and market position make it an attractive option for investors, there are also risks associated with investing in the company. Here are some of the key risks to consider:

- Legal challenges: Qualcomm has faced several legal challenges in recent years related to its business practices, including antitrust violations and patent infringement lawsuits. These challenges could potentially impact the company’s market position and future growth and result in high legal costs.

- Competition: The semiconductor industry is highly competitive, with many players vying for market share. While Qualcomm is a market leader in the mobile device and IoT markets, it faces stiff competition from other companies in the industry, such as MediaTek. As a result, Qualcomm could lose market share and revenue if it cannot innovate and stay ahead of the competition.

- Customer concentration: Qualcomm’s revenue heavily depends on a few key customers, including Samsung and Apple. If one of these customers were to reduce their reliance on Qualcomm or switch to a competitor, it could significantly impact the company’s revenue and profitability.

- The semiconductor industry is very cyclical. Therefore, analyzing the timing of different stages in the industry cycle is often the key for investors. Buying the stock at the cycle’s peak or at the wrong moment could lead to negative returns for investors for years.

Let’s make a quantitative and qualitative stock valuation, considering the strengths and risks mentioned so far.

A look at Qualcomm using the Everest Analyzer

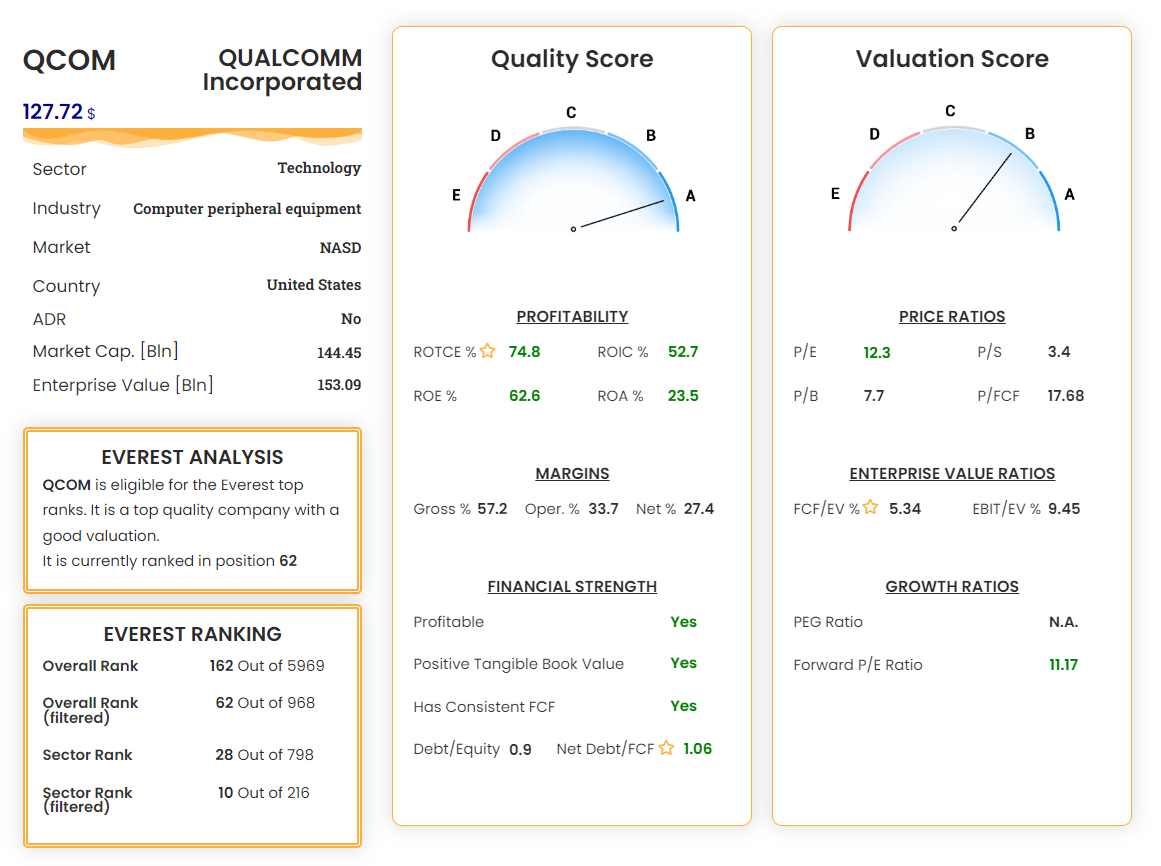

Quality Score: Qualcomm is a solid company with a management able to bring excellent profitability and margins. Profitability and margins are consistently better than the industry average. Its ROTCE of 74.8% is significantly over the industry median (43.8%) and the threshold of 35%, which the Everest Formula considers a good target value. The Everest Analyzer assigns a perfect score of A to its quality.

Valuation Score: Almost all the most important valuation metrics are better than the median of the Semiconductors industry: the P/E ratio of 12.3 is well below the median (18.6), and both EBIT/EV and FCF/EV are significantly better (9.45% vs. 5.62%, and 5.34% vs. 3.73%). Anyway, the FCF/EV is not high enough to consider QCOM a bargain from a valuation point of view. As a result, the Everest Analyzer assigns a score of B to its valuation.

Evaluation of Qualcomm through Discounted Cash Flow

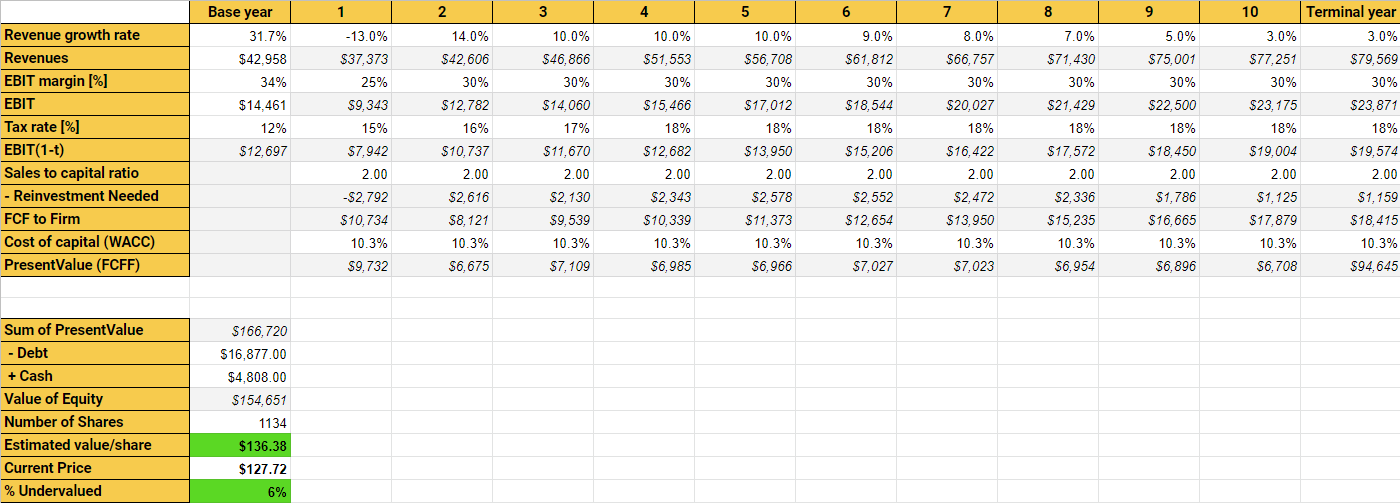

We proceed to analyze Qualcomm through a DCF model. Considering that this is a cyclical stock, the assumptions we will make need to be considered average values that could vary considerably from year to year.

Here are the assumptions we made considering the company’s strengths and weaknesses:

- Future Revenue Growth: QCOM expects to shrink its revenue next year due to the weaker demand and stabilize its revenue to 10% per annum for the following years before aligning with the average market growth at year 10.

- Future Operating margins: We assume that Qualcomm, after the expected headwinds, will maintain an average operative margin of 30%, in line with its recent past.

- Future effective tax rate: We assume that Qualcomm in the future will have an average tax rate of 18%, more than the last years but less than the average U.S. tax rate (21%).

- Future sales-to-capital ratio: We assume that Qualcomm will maintain an average sales-to-capital ratio of 2, in line with its recent past.

- Discount rate: We choose to discount the future cash flow with the Weighted Average Cost of Capital (WACC), which is the most reliable way to value a company because it considers its risks and the overall market outlook. We computed a WACC of 10.3% for Qualcomm.

With these inputs, we can estimate year by year the expected free cash flow generated by the company from year 1 to year 10, in which we assume to sell the stock. Summing up all these discounted FCF, subtracting debt and adding current cash, we obtain an intrinsic value for each share of 136.38$.

Given our calculations and the current price of 127.72$, the stock seems 6% undervalued. But given the uncertain nature of estimates and the need for an adequate margin of safety before buying a stock, we would prefer an undervaluation of at least 20% before considering Qualcomm a buy. So our buy price is currently 108$.

Here you can download the template used. You can modify the assumptions and extract your own intrinsic value.

Conclusions

We scoured the market for good deals and came across Qualcomm, an excellent company at a fair price, which should be on the watchlist of value investors. We would wait for a further 15% decline before considering it a buying opportunity. The Everest Formula is a successful investing strategy and a powerful stock analyzer that can be used to seek out value stocks in any sector and market condition.

So, what are you waiting for? Join our community!