- The Consumer staples sector is one of the best defensive sector to own during this high inflationary environment, because its companies operate in stable industries and sell products that are always in demand. Consumer staples companies have a better than average ability to pass on cost increases.

- In this article we are going to illustrate the advantages and risks of investing in this sector right now, and the best stocks that the Everest Screener suggests.

Are you interested in finding the best value stocks in each sector on your own? Premium members can use the Everest Screener to get the most valuable companies to invest in for each sector, everyday. Join now!

Consumer Staples – general overview

Consumer staples are bought everyday. They include daily essentials such as food and beverages, personal care products, household and home care products such as paper goods, and alcohol, tobacco, and cosmetics. These goods are bought regardless of the state of the economy, and the amount you buy is relatively equal in good and bad times. For these reasons the Consumer Staples Sector is considered the most defensive and resilient sector in a recession and during an high inflationary environment, like the current one.

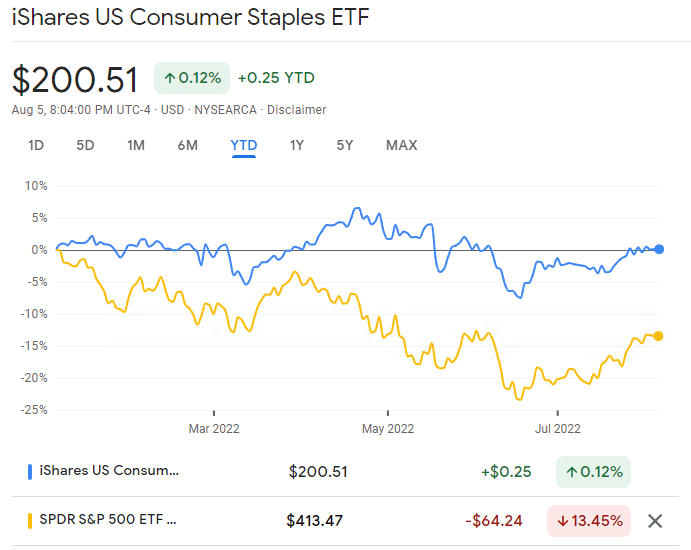

The iShares U.S. Consumer Staples ETF offers a great choice to expose to U.S. companies that produce a wide range of consumer goods, including food, and household goods, with all the advantages of an ETF, such as low costs, diversification, tradability, and liquidity. So far, in 2022, the Consumer Staples ETF has performed really well, keeping a positive performance despite the current bear market:

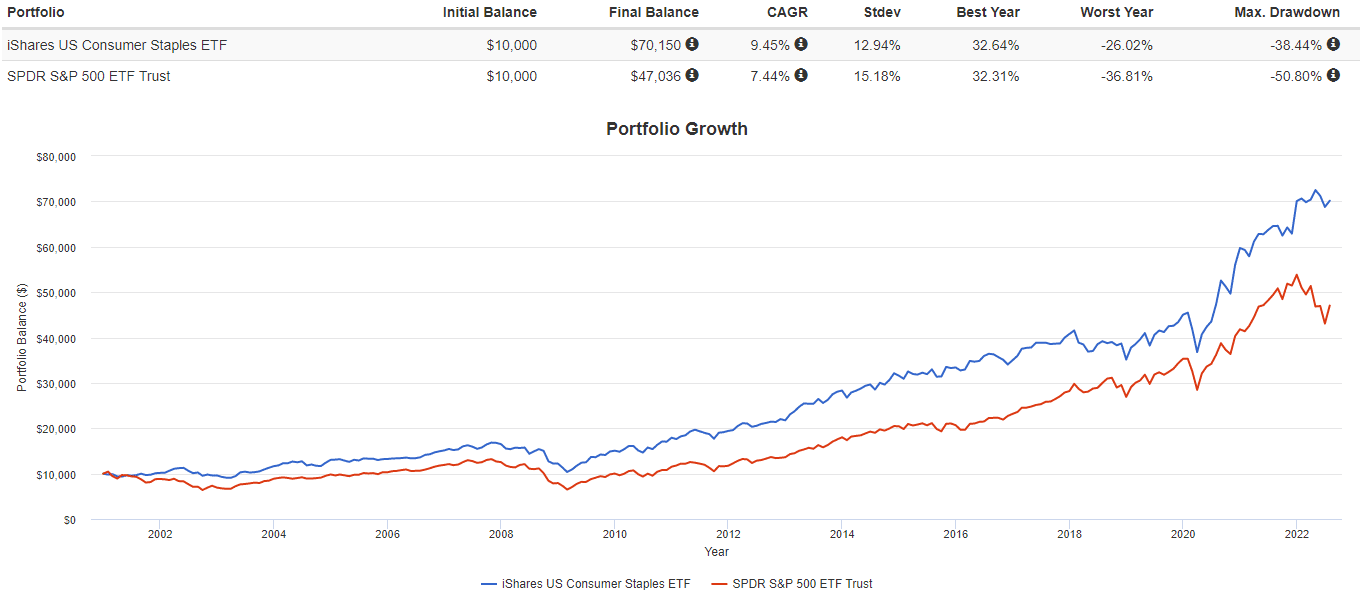

Even from a long-term perspective it has outperformed the market over the last 22 years, with the additional benefits of providing less volatility and cushioning losses during crashes:

Sector Advantages

- Consumer Staples has proven to be a defensive sector: Since 2000, Consumer Staples companies have weathered much better than the overall market during major crashes. These companies sell goods such as food and cleaning products that consumers rely on regardless of the state of the economy; they tend to generate solid profits even in weak economies.

- It’s a good hedge against inflation: Basic goods demand is immune from inflationary pressures. Consumer Staples companies can increase prices without incurring a drop in sales.

- High dividend yields: Consumer Staples stocks are often popular with retirees and other investors seeking long-term income and security. Many offer better dividend yields than an S&P 500 ETF.

Sector Disadvantages

- Low growth: Consumer staples companies may not have the highest earnings growth or year-over-year revenue growth because these stocks tend to be large, mature companies. Is an unsuitable sector for those seeking an high-risk-high-reward portfolio.

- Consumer Staples sector tends to underperform during strong markets: If inflation subsides and the economy rebounds strongly, a stable and low-growth sector such as the Consumer Staples will lag behind more volatile sectors such as Consumer Discretionary and Technology.

So, how can we take advantage of the benefits of this sector without risking poor future performances? We need to select the right stocks within this sector. Stocks that are undervalued, highly profitable and well managed at the same time. Here the Everest Formula comes in handy.

We’ll show the best stocks of the Consumer Staples sector picked by our algorithm, that can be analyzed more in depth, seeking out possible bargains.

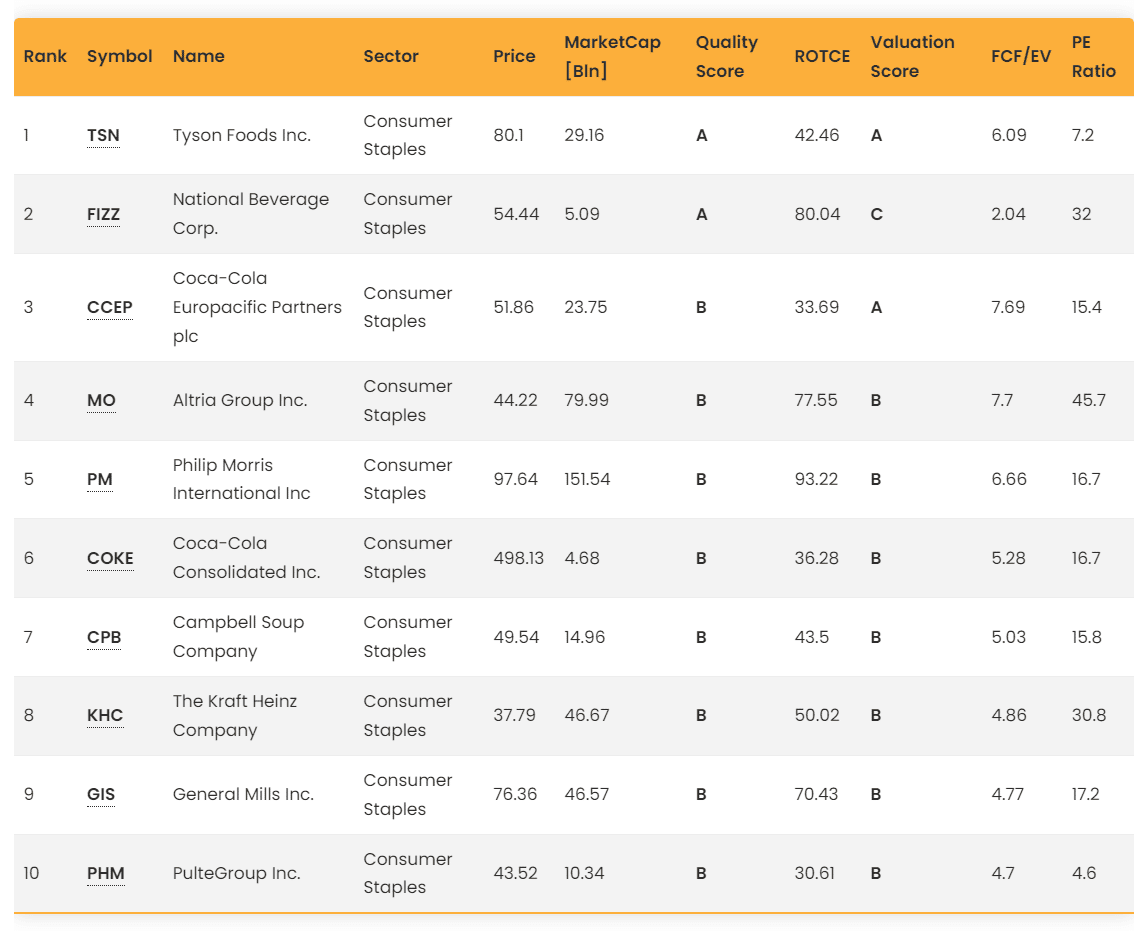

Top 10 stocks of the Consumer Staples Sector

These are the most interesting stocks that Everest Formula suggests in the Consumer Staples Sector, as per today:

We are going to analyze the first 4 stocks of the rank. For each stock, we will look at the Everest Analyzer to have an overview of the stock metrics, and we will do a discounted cash flow (DCF) valuation to discover possible bargains.

Note: For the DCF valuations, we will use the following data:

- The base year data, that are extracted from the last earning report of each company.

- The expected future revenue growth, EBIT margins and tax rates, that are taken from the analysts forecast.

- The Sales/capital ratio. We will use the industry average.

- A discount rate of 7.8%, made of the current risk free rate (2.8%) plus a standard equity risk premium of 5%.

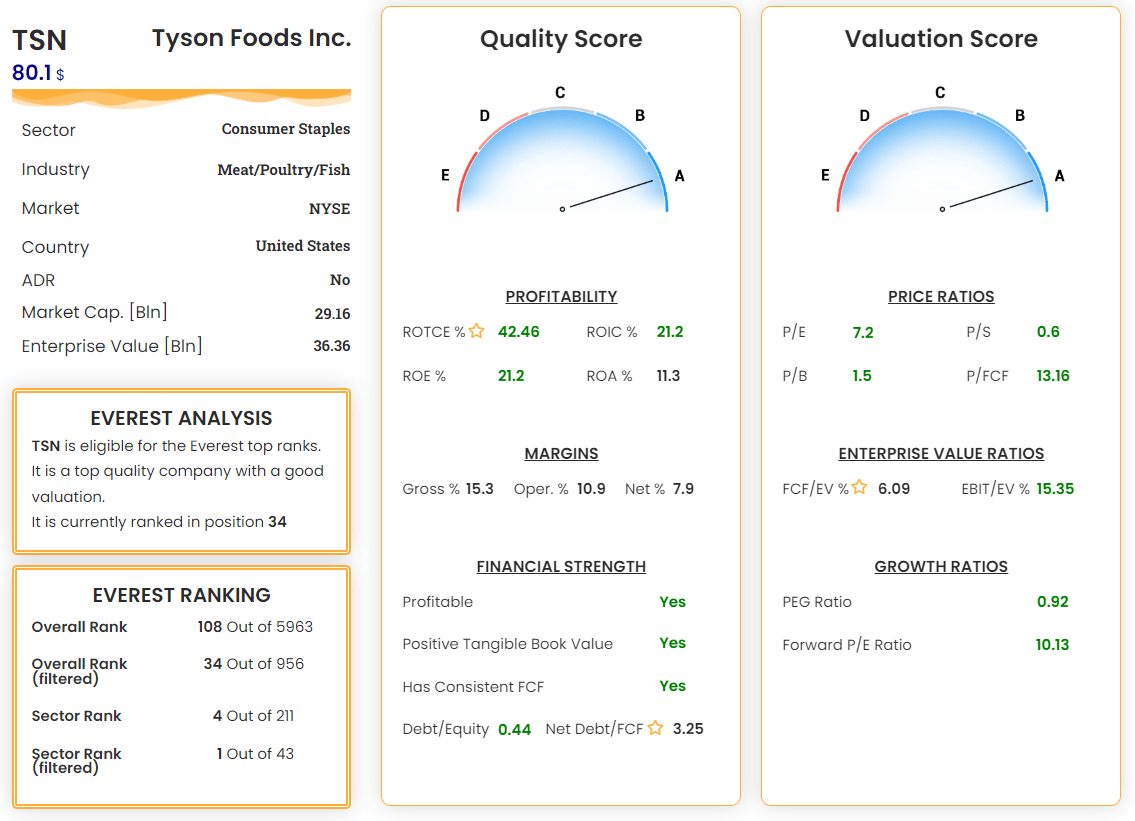

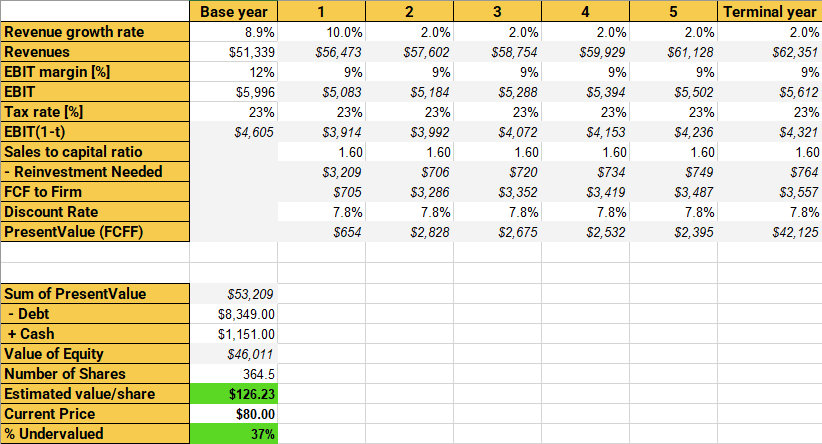

1) TSN – Tyson Foods Inc.

Tyson Foods Inc. is a big supplier in the global food market. They sell beef, pork, and chicken as well as their own packaged foods with brands like Tyson, Jimmy Dean, Hillshire Farm, and Ball Park. The company is in what many would consider a boring industry because they sell processed proteins and it will always have demand but not sky high growth rates. The financial results for 2022 are good and the company anticipates strong performance throughout the rest of the year.

The company is well positioned for continued earnings growth in the future. They are the market leader in many key retail categories and have room to grow in these product areas. They have plans to open 12 plants within the next 2 years to increase capacity by around 1.3 billion pounds. Most of these plants are in international markets where the companies can see further growth opportunities in the future. As well as a few domestic plants coming online in the United States.

Risks: Decreasing volumes is the main risk for Tyson Foods. The growth in population will drive demand forward, but a steep increase in interest in plant-based diets can accelerate this risk. Adding vegan options and improving the efficiency within the meat segments takes time, and challenging is the process in itself. A successful process will unlock value, but a slower process may turn investors more skeptical and lower the valuation.

Valuation: TSN has a really high profitability and good management able to produce a lot of free cash flow whilst keeping the debt low. Moreover, it as an attractive valuation, with a PE ratio of only 7.2 and a good FCF/EV of 6.1. Everest Formula assigns to TSN a perfect score of A, both on the quality and on the valuation.

Even the DCF model confirm that the stocks is currently 37% undervalued. TSN is one of the best bargain in the Consumer Staples sector right now.

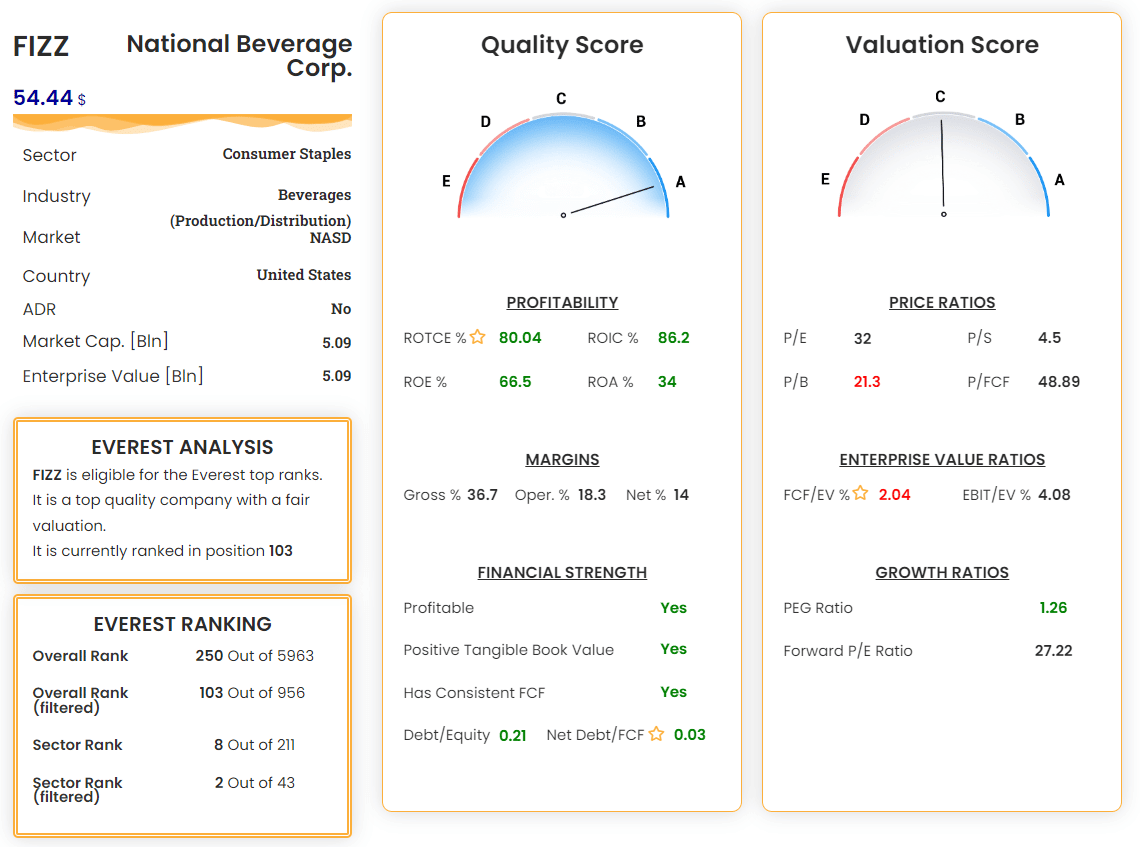

2) FIZZ – National Beverage Corp.

National Beverage Corp. is quite a small beverage company that owns some important brands like LaCroix, Everfresh, Clear Fruit and Rip It. To service several thousands of customers, the company operates 12 production facilities located in 10 different states.

In recent years, the company has demonstrated reliable growth on its revenue (6% CAGR) plus consistent and generally growing cash flows on net income (8% CAGR). This year, the business looks set to continue on that trend.

Risks: National Beverage looks to be a sturdy and reliable enterprise. The company has a very low level of risk associated with it. However, growth, while positive, has not been all that strong. The major risk of FIZZ is buying it at a too high price, limiting the future stock performance.

Valuation: the Everest Formula confirms the really high quality of the business, an astounding ROTCE and ROIC, great margins and virtually no debt. despite that, the valuation seems not so good: the PE ratio of 32 is a bit high and the free cash flow is not enough to justify its enterprise value.

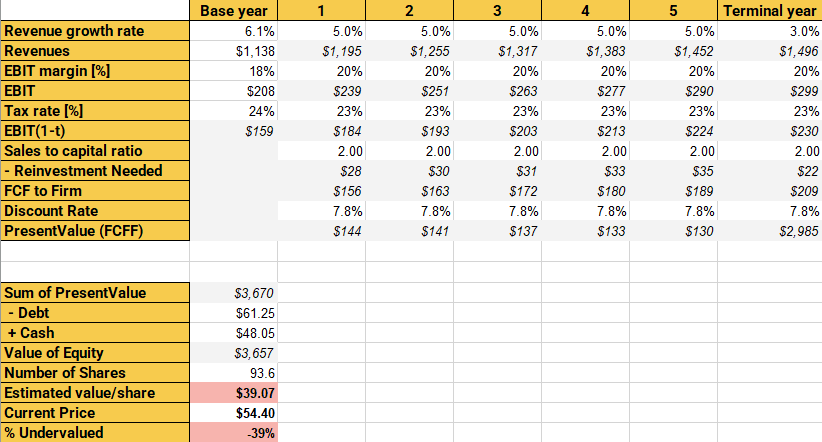

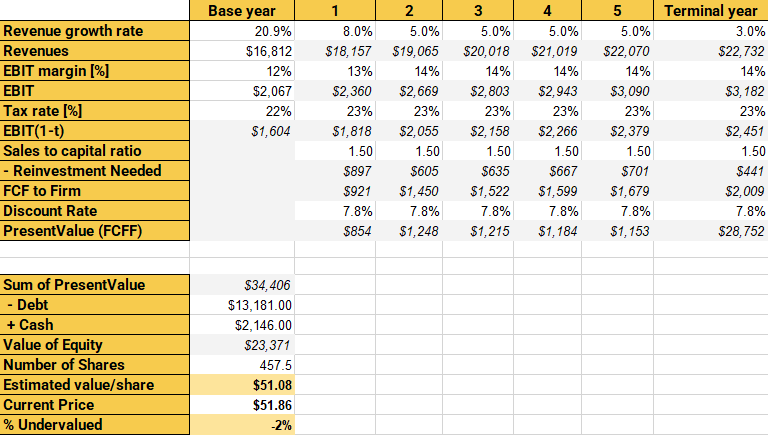

The DCF model computes an intrinsic value of 39.07, 39% lower than the current price. We would wait a price decrease before considering FIZZ a buy.

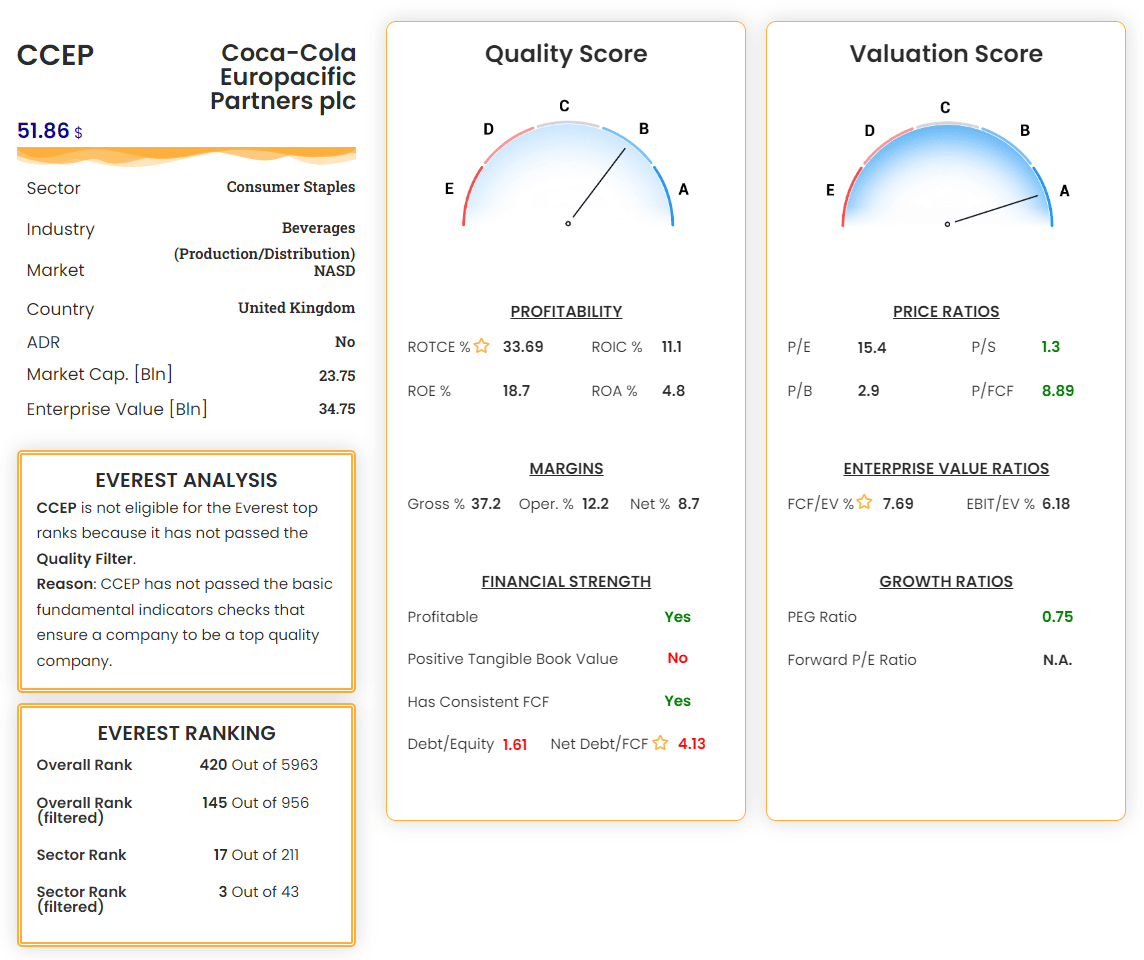

3) CCEP – Coca-Cola Europacific Partners plc

CCEP is a bottler producer company that produces and bottles the finished product of the parent Coca-Cola Company. CCEP offers investors exposure to a large Coca-Cola bottler across Europe and Asia Pacific. The business is performing solidly, with revenues growing strongly. The dividend yield looks particularly attractive at the moment.

CCEP has been heavily affected by COVID. 45% of the company’s pre-pandemic sales were attributable to the away-from-home channel, and its territories were among the harshest in terms of lockdown measures, severely affecting on-trade venues like restaurants, pubs, hotels and so on. 2021 saw the expected recovery, albeit that recovery is progressing slowly as many territories maintained significant restrictions, especially in the first half of the year.

Risks: Looking ahead, there are some headwinds to consider. The company is facing a secular headwind in terms of increasingly health-conscious consumers turning away from sugary carbonated drinks. Secondly, the MOAT is not as strong as the parent company, and the competition with other bottlers could limit its growth.

Valuation: the Everest Analyzer outlines a good profitability and margins. The debt is a bit too high but is mostly related to the asset-intensive business in which CCEP operates. The valuation metrics are good, with an actractive PE of 15.4 and a FCF/EV of 7.7.

Using the DCF model with the analysts estimates, CCEP seems correctly valued at the moment. CCEP could be a nice investment, but not a bargain now.

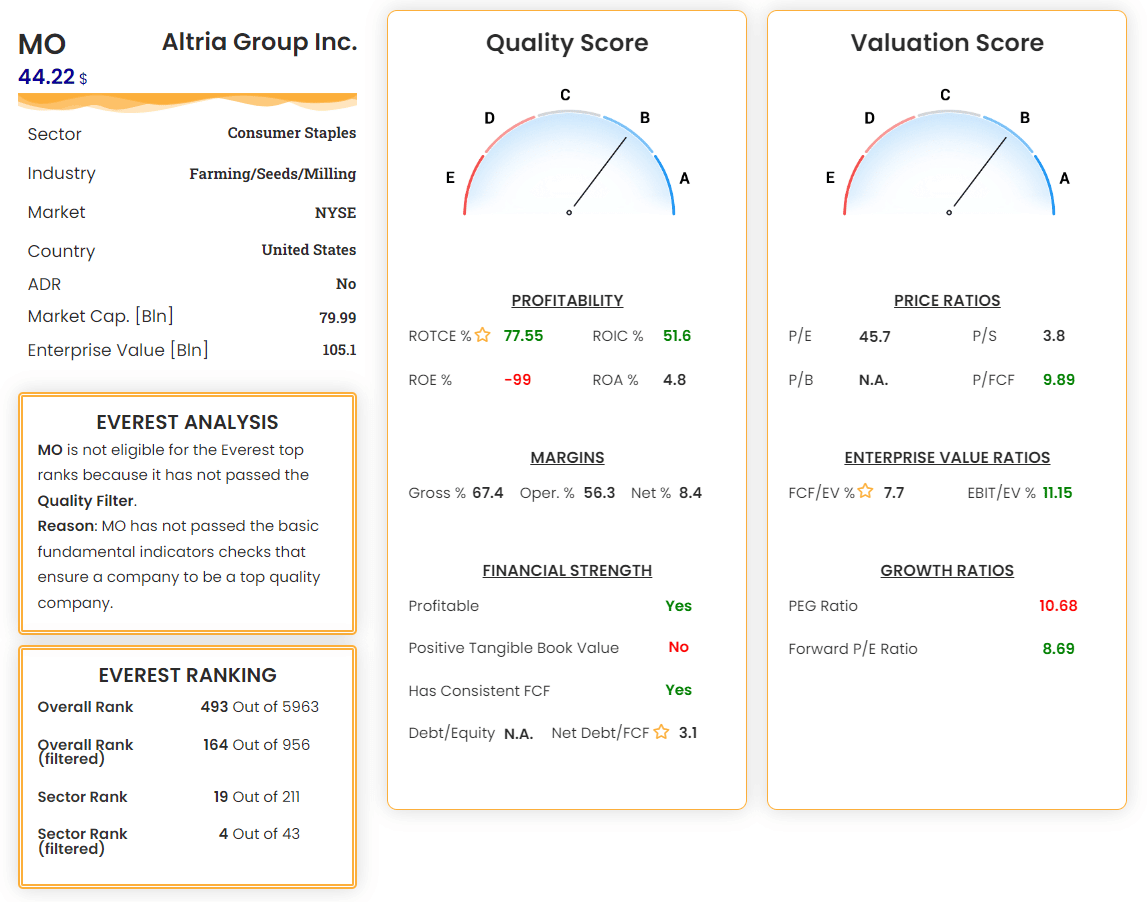

4) MO – Altria Group Inc.

Altria Group manufactures and sells smokeable and oral tobacco products in the United States. The company provides cigarettes primarily under the Marlboro brand, plus cigars and pipe tobacco principally under the Black & Mild brand. Altria has been founded in 1822 and has always been demonstrated to be a solid defensive play in recessions. MO pays high, generally sustainable dividend yields and might be considered in a well-rounded portfolio.

Altria’s shares recently fell after the FDA has banned all of Juul Labs’ vape products (owned by Altria) from the U.S. market. But even without Juul products, The U.S. tobacco market is expected to grow at a 3.4% CAGR to reach $102.70 billion by 2030.

Risks: The tobacco industry has always been subject to increasing legislative restrictions by governments, that could limit the profits and gradually brings to a revenue decline in the next decade.

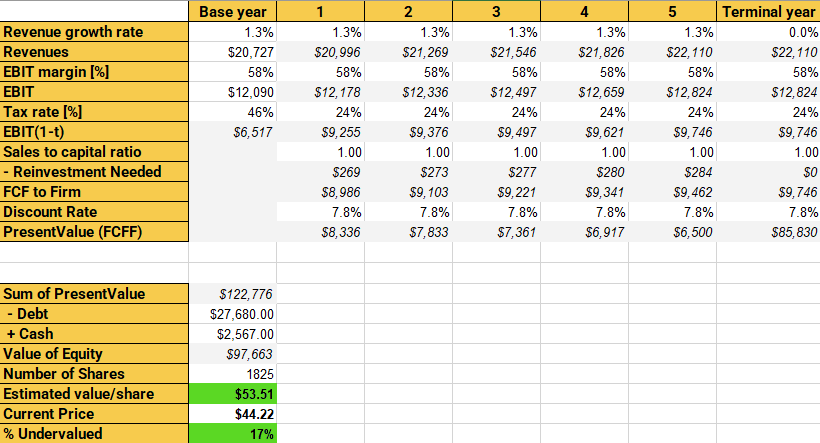

Valuation: MO has a good profitability and a contained debt, together with an intriguing valuation. The DCF valuation confirm that MO could be a good investiment with a potential upside of 17% from the current price, should the analysts estimates be confirmed.

Conclusions

The consumer staples sector could be the right sector to invest in if the current scenario of economic slowdown and high inflation will prolong in the coming months or even years. The Everest Formula has been a great tool for identifying the best opportunities in the industry, one among them Tyson Foods Inc. The Everest Formula is a powerful algorithm that can be used to seek out value stocks in any sector and any market condition.

So, what are you waiting for? Join our community!